Growth versus Value Stock Investments

If you are like many architects, you understand the value of saving for the future and proactively contributing to your retirement accounts.

Text

If you are like many architects, you understand the value of saving for the future and proactively contributing to your retirement accounts. As a firm owner or as an employee of an architecture firm, there are many retirement savings options such as a 401(k) plan or an IRA product. But once retirement assets begin to build, many architects have questions on the most effect strategies for investing.

It’s important to understand a key distinction in equity investing: growth and value. Understanding these styles of equity investment will allow you to determine how they may impact your investment objectives. These equity investment choices should be considered along with assessing your risk tolerance, investment objectives and your retirement horizon.

Growth and value are two fundamental approaches in stock and mutual fund investing. Many growth stock mutual fund managers look for stocks of companies that they believe offer strong earnings growth potential, while value fund managers look for stocks that appear undervalued by the marketplace. Some fund managers combine the two approaches.

How to identify growth and value stocks

While earnings of some companies may be depressed during periods of slower economic growth, growth companies generally seek to achieve high earnings growth regardless of economic conditions. “Emerging” growth companies are those that may have the potential to achieve high earnings growth, but have not yet established a history of strong earnings growth.

Value stocks are those that have generally have fallen out of favor in the marketplace and are considered bargain-priced compared with book value, replacement value, or liquidation value. Typically, value stocks are priced much lower than stocks of similar companies in the same industry. This lower price may reflect investor reaction to recent company problems, such as disappointing earnings, negative publicity, or legal problems, all of which may raise doubts about the companies’ long-term prospects. The value group may also include stocks of new companies that have not been recognized by investors.

The primary measures used to define growth and value stocks are the price-to-earnings ratio (the price of a stock divided by the current year’s earnings per share) and the price-to-book ratio (share price divided by book value per share). Growth stocks usually have high price-to-earnings and price-to-book ratios, which means that these stocks are relatively high-priced in comparison with the companies’ net asset values. In contrast, value stocks have relatively low price-to-earnings and price-to-book ratios.

Features of growth and value stocks

Growth Stocks

- Higher priced than broader market

- High earnings growth records*

- Less sensitive to economic conditions than broader market

Value Stocks

- Lower priced than broader market

- Currently priced below similar companies in industry

- Carry more risk than broader market

* Past performance is not indicative of future results.

Growth and value: complementary investment styles

Following a specific investment style, such as growth or value, provides investment managers with guidelines for choosing stocks. Growth fund managers look for high-quality, successful companies that have posted strong performance and have expectations to likely continue to do well, though there are no guarantees. Of course, there is no assurance that this forecast will be attained. Investors are willing to pay high price-to-earnings multiples for these stocks in expectation of selling them at even higher prices as the companies continue to grow. The risk in buying a given growth stock is that its lofty price could fall sharply on any negative news about the company, particularly if earnings disappoint Wall Street.

On the other side, value fund managers look for companies that have fallen out of favor but still have good fundamentals. They buy these stocks at prices below the stocks’ average historic levels or below the current levels in their industry groups. Many value investors believe that stocks become value stocks when investors overreact to negative events. The idea behind value investing is that stocks of good companies may bounce back in time when the true value is recognized by other investors. But this recognition of value may take time to emerge and, in some cases, may never materialize.

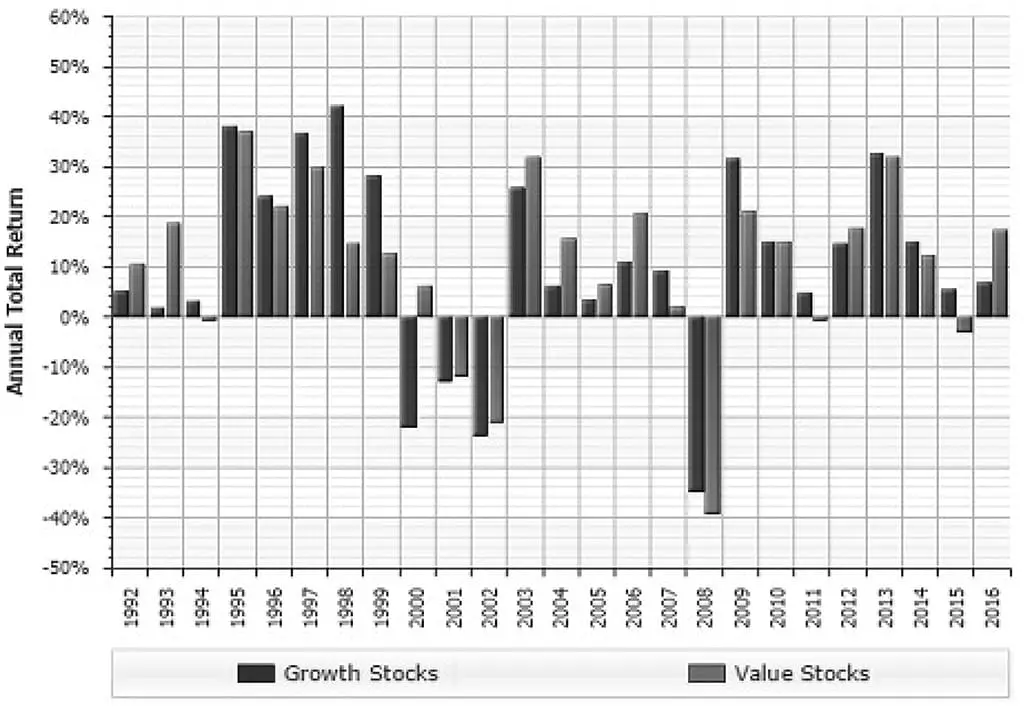

Which strategy—growth or value—is likely to have higher return potential over the long term? The battle between growth and value investing has been going on for years, with each side offering statistics to support its arguments. Some studies show that value investing has outperformed growth over extended periods of time on a value-adjusted basis. Value investors argue that a short-term focus can often push stock prices to low levels, which, in turn, can create great buying opportunities for value investors.

Growth vs. value: compare the performance

Manage risk by combining growth and value

For many mutual fund investors, however, there may not be an absolute advantage to any single approach to investing over a long period of time. Instead of choosing only one approach, individual investors may strive for the best-possible returns while managing risk by combining growth and value investing. This approach allows investors to potentially gain throughout economic cycles in which the general market situations favor either the growth or value investment style.

For example, value stocks, often stocks of cyclical industries, generally tend to do well early in an economic recovery while growth stocks, on the other hand, tend to lead bull markets which are normally fueled by falling interest rates and increased company earnings. Also, because the two groups of stocks tend not to move in the same direction or to the same extent, investors can potentially enhance returns and manage risk by combining the two approaches.

The AIA Trust is here to help

The AIA Trust offers retirement savings and distribution vehicles through AXA Equitable to assist you in achieving your retirement goals. Plans can be established for one-person firms—or for many employees—utilizing a variety of retirement savings and distribution vehicles. AXA Equitable can assist you in achieving your goals based on 50 years’ experience working with association members and over 25 years with AIA architects. AXA Equitable can help you review your options and offer you choices that will alleviate the burden of establishing and managing a retirement savings plan. It’s one of the ways that the AIA Trust makes it easier for you to focus on doing what you do best: architecture.

Call (800) 523 1125 to speak with a Retirement Program specialist or learn how you can start saving today.

This article has been written for general information purposes only. This material does not constitute an offer or solicitation of any kind and is not intended, and should not be relied upon, as investment, tax, legal, or financial advice or services.

The Members Retirement Program contract form #6059 is funded by a group variable annuity contract issued and distributed by AXA Equitable Life Insurance Company, NY, NY. Annuities have limitations and restrictions. For costs and complete details contact a Retirement Program Specialist. AXA Equitable and its affiliates do not provide tax or legal advice. You should consult with your attorney and/or tax advisor before purchasing a contract.

© 2018 DST Systems, Inc. Reproduction in whole or in part prohibited, except by permission. All rights reserved. Not responsible for any errors or omissions.

Please always consider the charges, risk, expenses, and investment objectives carefully before purchasing any financial product, including mutual funds or variable annuities. For a prospectus containing this and other information, please contact a financial professional. Read it carefully before you invest or send money.

AXA Equitable Life Insurance Company (NY, NY) issues life insurance and annuity products. Securities offered through AXA Advisors, LLC, member FINRA, SIPC. AXA Equitable and AXA Advisors are affiliated and do not provide legal or tax advice.

GE-2123252 (6/18)(Exp. 6/20)

More on Retirement & Financial Planning

Charitable Contributions: Five Frequently Asked Questions

News ▪ January 2026

Don’t Underestimate Health Care Costs in Retirement

News ▪ October 2025

Mastering Financial Planning for the Sandwich Generation

Retirement & Financial Planning ▪ Trust Week ▪ Webinar